Dell Shareholders Approve Buyout

So, barring any last-minute heroics from unknown parties, it looks like the original deal proposed earlier this year is going down largely unchanged from its original terms. This leaves us with a lot of things to ponder going forward about the business of being an IT infrastructure player. As I blogged previously, the deal also presents an interesting barometer of risk tolerance in the post bubble, post-2008 world. Finally, there's the fact that corporate raiders... err, I mean activist shareholders... seem to have jumped the shark with this deal.

Let's deal with Icahn first, since he has been an endless source of amusement for me. I love, love, LOVE it when a guy like him parrots democratic principles while trying his best to squeeze money out of anyone he can. One thing that I have learned over the years is that a corporation is anything but a democracy. Frankly, large or small, its much closer to a dictatorship when it works best. There is one important distinction: if you are an employee, customer, stockholder, or all of these, you can feel free to walk away at any time. You can even sell the stock short and say mean things on message boards. Except for that, it's just a matter of scale. Are we with Fidel, Saddam, or Lenin? The notion that the shareholders can tweak management is valid only on the margin and in extreme cases. Maybe you can argue that Dell was such a case, but, as you can see, it was very easy for management to do what they saw fit. Management sets the rules, and then can change them as is expedient. If you want to fire them all, you best have a plan to replace them quickly, lest you become the guy that has to run the place.

Which segues into the second point: Icahn clearly never wanted to buy Dell. He never had the money to buy Dell. Even if he had the money, he had no credible plan to rehabilitate Dell. Heck, I'd be astonished if he could carry Michael's briefcase successfully. When Blackstone bowed out earlier this year, he had an opportunity to gracefully leave the table with a profit, and spare himself the embarrassment of last week. If he really believed in the value proposition of owning a private Dell, he could have toned down the incendiary rhetoric, and tried to roll his position into a stake in the new entity. There were so many ways to win... Instead, he lost a very public battle in a circus setting of his own creation. As a result, everyone now knows what his credit limit is. Everyone now knows when he's in over his head. He's going after Apple now, which is 20 times the size of Dell. I wonder how worried the guys in Cupertino are these days.

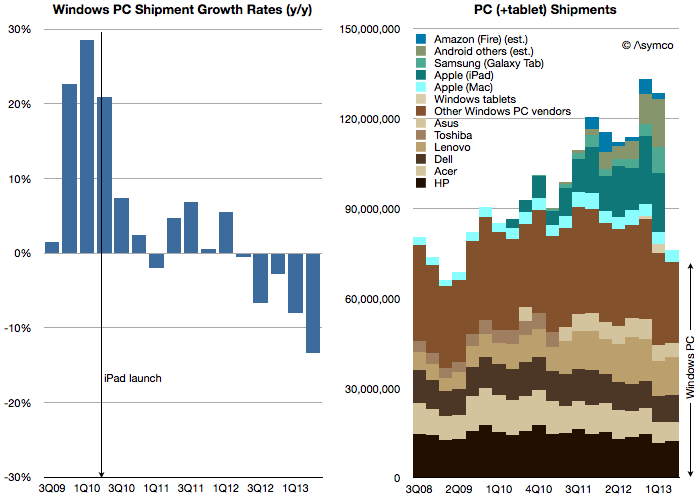

All that said, there is a special corner in Hell being reserved for the people that have to carry on in the private entity about to be created. The vast majority of the revenue, the supply chain, and the employee base are tied to a product stream that is in secular decline. The rumors are that they are thinking about a $2 billion cut in operating expenditures. (read massive layoff) As I have blogged previously, searching for loose change underneath the drivers' seat is no substitute for actually taking the wheel and trying to go somewhere. Meanwhile, Horace Dediu puts together some charts that tell a damning story about where the car is going:

What happens if sales keep declining? More cuts, maybe? What part of that growing market for Android, and iOS mobile devices does the Intel/Microsoft/Dell troika have? Let's ask the bigger question: How much is Dell really going to invest to keep a share of this market, and why do they keep talking about it so much? One thing is certain: If they are going to ramp up that enterprise business to replace client revenue, it will take a herculean investment to even get things close. The strategy of making small purchases to grow the business will not yield results quickly enough, nor is the prospect of having to integrate and manage all those organizations a particularly easy path. One is left to wonder if there aren't one or two really big transactions to follow this one. Then again, they are a private company now. Does it really matter any more?

With that, off to hit the scotch...

No comments:

Post a Comment